Posts filed under ‘Economics’

Advice from a 93 year old

No, it’s not me giving the advice. A couple of more years to go before I hit 93 years :)- I found this article in Time really interesting – it’s an interview with a 93-year old economist, Anna Schwartz. Now, the most amazing part of this interview for me is that it seems Anna Schwartz is STILL working (as an adjunct professor at the Graduate Center of the City University of New York and from what I’ve read, as an economist). This is no old goat speaking about ‘when she was young” because she has some serious chops.

No, it’s not me giving the advice. A couple of more years to go before I hit 93 years :)- I found this article in Time really interesting – it’s an interview with a 93-year old economist, Anna Schwartz. Now, the most amazing part of this interview for me is that it seems Anna Schwartz is STILL working (as an adjunct professor at the Graduate Center of the City University of New York and from what I’ve read, as an economist). This is no old goat speaking about ‘when she was young” because she has some serious chops.

Anna Schwartz lived through the Great Depression that started in 1929; she co-authored with Nobel laureate, Milton Friedman, the highly acclaimed financial bible A Monetary History of the United States (Princeton University Press, 1963); she’s been studying recessionary patterns for decades; and she’s worked as an economist with the National Bureau of Economic Research in the US since 1941. You can read the full interview here but I’ll give you a taste of her words of wisdom when asked about our current global financial woes.

- the Obama Administration should stop bailing out corporate disasters and abandon plans to move health care onto the backs of taxpayers. Bailing out corrupt corporates just leads to them continuing their dodgy practices and putting out their hands for more Government bailouts if you ask me.

- Schwartz believes that the bottom of the recession will be hit sometime during the (US) Spring of 2009. But recovery will not be in leaps and bounds because consumers are saving and not spending.

- she doesn’t think much of Obama’s fiscal stimulus package and thinks the Feds should print more money.

- if a financial institution or company is having financial woes, it should be encouraged or even compelled to file for bankruptcy. And If GM was on the verge of bankruptcy, it should have been shut down.

- Obama’s health care reforms – Schwartz believes that the trouble with Obama’s plan is that he has no concept of the cost that will be imposed on the economy if his program is enacted.

- It was the Government’s program to promote home ownership that permitted all the excesses that occurred over the years. People who should never have been granted a mortgage were given one.

- there’s been a lot of talk about helping stop foreclosures and Schwartz suggests that if the Government has a program that will help to stabilize the housing industry, then this will improve chances for a revival of the economy.

It’s a very interesting interview. And from the perspective of knowledge management, here’s someone with a wealth of expertise and lessons learnt – Prez Obama should perhaps listen.

Photo: source

Some simple questions

The United States has spent US $11.6 trillion (and counting) on bailouts and stimulus packages. Click here to see how the US Government has used taxpayer dollars. The Australian Government has coughed up AU $42 billion so far – to get people spending on retail goods, to fund infrastructure spending and building works at schools. Mind you, it seems that a whole lot of dead people benefited from the $900 handout too (around 16,000 individuals) along with people with an overseas residential address in countries like the UK, US, France, Germany and Brazil. Talk about a waste of taxpayer’s hard-earned dollars.

The United States has spent US $11.6 trillion (and counting) on bailouts and stimulus packages. Click here to see how the US Government has used taxpayer dollars. The Australian Government has coughed up AU $42 billion so far – to get people spending on retail goods, to fund infrastructure spending and building works at schools. Mind you, it seems that a whole lot of dead people benefited from the $900 handout too (around 16,000 individuals) along with people with an overseas residential address in countries like the UK, US, France, Germany and Brazil. Talk about a waste of taxpayer’s hard-earned dollars.

Meanwhile, GM and Chrysler bite the dust, filing for Chapter 11 bankruptcy and leading to unemployment for tens of thousands. In the United States, 14.5 million people are looking for work; in Australia, the jobless rate is around 5.7% and predicted to rise to 8.5% over the next 12 months as Australia starts to feel the ferocious bite of the GFC (although we had a positive growth quarter in March). State governments are running out of money – just look at California, a US state that is taking a real beating. Tax refunds, welfare cheques and student loans were suspended from February 1, 2009 as the State had no cash. At least 43 US States are struggling with budget shortfalls. And in Australia, we’ve just heard the news that our universal free health care system may no longer be free within five years, leaving sick people to be – well, sick – if they can’t cough up the money to pay for health care.

When you read about the likes of AIG having the hubris to pay senior employees millions of dollars in bonuses after receiving US$165 million in federal aid, you have to start asking some very simple questions. Not pointy-headed economic questions, just simple ones like:

- how are governments going to provide for the unemployed? help them to survive and not be stripped of dignity? how will the homeless be given shelter and fed?

- what happens when State governments run out of money, to the extent that the elderly and sick are not cared for?

- how do we regulate the economy and get governments to step in and address market failure? (basically a return to Keynesian economics)

- should we be reversing the privatization of infrastructure and banks? The three hallmarks of privatization are divestiture, deregulation and outsourcing and look at where this has got us – concentration of wealth; the stripping of public resources; social objectives subordinate to the profit motive; private companies making a profit and serving the needs of those who can or are willing to pay the most, whilst the needs of the majority are not forefront – this is undemocratic. And the thing I really fear is the privatization of water – there would be no guarantee that water could be delivered safely to the public at an affordable price. And if you can’t pay for water, you will be denied a basic human right.

- what are governments going to tell the elderly and the sick or youth who will be expecting jobs? – oops, sorry, we spent all your taxpayer dollars and can’t help you.

- how do we rebuild a sense of community and neighbourliness in our society? if we can’t look to government to support us now in this financial mess or in the future because we’ll be saddled with government debt – how do we help ourselves and others?

- how are we going to avoid or cope with civil unrest? The GFC is causing hardship; there is anger against Wall Street; millions are losing jobs; more people are homeless; we are wary about being burdened with government obligations that may take generations to repay.

And it’s pretty clear that governments are bracing themselves for civil unrest. Let’s look at some examples:

- the CIA has added the economy to its daily security briefing for the White House – looking at the GFC and its cascading effects on the stability of countries throughout the world;

- in the UK, MI5 has plans to cope with civil disorder and the army is on standby. The DCDC (Development, Concepts & Doctrine Centre, UK Ministry of Defense) warned in 2007 in their strategic trends report (p81) that: “the middle classes could become a revolutionary class….The growing gap between themselves and a small number of highly visible super-rich individuals might fuel disillusion with meritocracy, while the growing urban under-classes are likely to pose an increasing threat to social order and stability, as the burden of acquired debt and the failure of pension provision begins to bite”.

- and I’ve told you before about H.R. 645, which established FEMA camp facilities on military installations in the United States – these centres would be used to provide temporary housing, medical and humanitarian assistance in the event of a national emergency eg civil unrest

- I’ve also told you before about a US Army think tank report – Known Unknowns: Unconventional “Strategic Shocks” in Defense Strategy Development – and on p32 of this report it says: “Widespread civil violence inside the United States would force the defense establishment to reorient priorities….to defend basic domestic order and human security. Deliberate employment of weapons of mass destruction or other catastrophic capabilities, unforeseen economic collapse, loss of functioning political and legal order, purposeful domestic resistance or insurgency, pervasive public health emergencies and catastrophic natural and human disasters are all paths to disruptive domestic shock”.

So if we put all of this together, what do we have?

- when we all realise that the bailouts and stimulus packages have failed to correct rampant capitalism and we are all laden with increasing taxes to prop up ailing governments – we will wake up and say we’ve had enough;

- when people can’t afford to pay for health care; when the elderly do not get pension support; when an urban underclass is saddled with debt – there will be civil unrest;

- when the future is one of food scarcity and water wars – there will be civil unrest;

- and when that time comes, the military is ready and able to step in and take control.

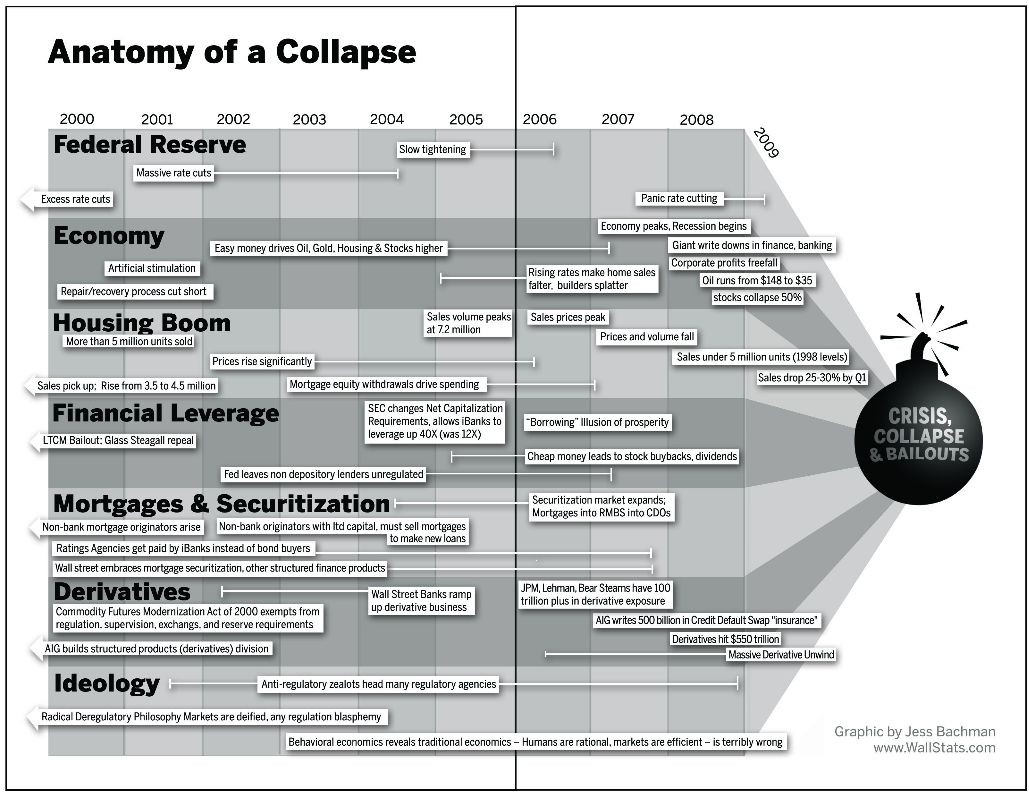

Anatomy of a collapse

Came across this great visual that seeks to explain our current predicament – the global financial hissy fit as I call it, or GFC. Barry Ritholtz has written a book that I’ve yet to read – Bailout Nation. And he wanted to visually describe all the factors that led up to the GFC. So he asked Jeff Bachman of Wall Stats to whip up a visual (Wall Stats is a great site that uses visuals to synthesise and portray complex information) and voila: 7 Factors that Led to Crisis:

Go here for the BIG picture.

Splashing the cash

So the Australian Federal Government is throwing squillions of dollars at stimulus packages, hoping to tempt consumers to spend up and give the retail industry a boost; increased infrastructure spending is proposed and AU$900.00 bonuses for qualified people have been handed out in an attempt to avoid a long, slow, painful recession (well, heck, let’s just admit it – AUSTRALIA IS IN RECESSION). Where is this money coming from and for how long can the Rudd Government keep throwing money at failing industries and households (who most likely squirrel any bonus payments into their bank accounts rather than shopping until they are dropping). As I understand it, to finance Government spending on infrastructure, bailouts and stimulus packages, it has three ways to get its hands on money:

- selling Australian Government bonds. These are attractive to buyers because when they mature, the principal sum is guaranteed by the Commonwealth Government;

- borrowing overseas capital from say the IMF or Asian Development Bank; and

- importing capital from a foreign country

But the global financial hissy fit is shrinking capital flow leading to a global solvency problem. Banks are reluctant to lend money as they stagger under the weight of financial losses on real estate. I read somewhere that the amount of money banks have in reserve that is non-borrowed funds is at a 50-year low.

Won’t this mean two things for Australia – humongous national debt and a capital flow crisis because we won’t be able to find overseas capital? I heard on a TV program that our national debt will mean that every Australian will “owe” $10,000 each. Our Finance Minister, Lindsay Tanner, said the other day that the government’s deficits would exceed a total of $100 billion over the next three years. Crikey! And how will the country get out of debt? Well, surely that means raising of taxes and interest rates or less government spending or both. Rudd has hinted that the rich might get slugged with a higher tax rate (following the UK’s lead). And if taxes go higher and the banks raise interest rates, then this means the bonus payments to Australians who qualified will eventually get paid back to the Government! So I’m getting concerned about what is quite clearly a debt binge that’s going on and I wonder if our Government shouldn’t be thinking of something else.

Rather than throwing $42 billion at stimulus packages that may or may not work, my view is that when a nation is in deep crisis, a responsible Government should do two things:

(1) baton down the hatches and prepare for a rough ride. After all, the IMF has just released its World Economic Outlook (grim reading) and expects the Australian economy to contract by 1.4% in 2009 and unemployment to rise to 7.8% by 2010. So it’s no good doing the PR spin and talking about how Australia will be largely shielded from the global financial hissy fit because we’ve always been the “lucky country”. The fact is we’re in the pickle with the rest of the world, so let’s admit it and get on with it. And getting on with it in my view means that the Government should be providing for its citizens to weather the storm – forget job creation, this is about survival and means providing housing, shelter, health care and transport, income support for those most severely affected. Then…..

(2) think about how to position Australia so that when the hissy fit is over, this country and Australians are ready and able to bolt out the gates and not be held back by a sluggish recovery. I think this means the Government taking over a lot of things – the banking system, infrastructure such as communications and rail transport that have been privatised. I have never been convinced that privatization of public utilities has increased competition (the raison d’être for privatization) and I think it is against the public interest. It is no longer about “serving the public” when something is privatized it’s about “getting profits and paying humongous salaries to CEOs” (and you finance the CEO salaries by raising prices).

So I think the Government needs to consider the following:

- the first home owner’s grant of $14,000 – I get that the Government is trying to encourage young people to buy their own home. But how about tying this grant to the condition of ensuring that the home is sustainable. Not the McMansion that takes up a whole block of land but a home that has energy efficient insulation, energy efficient lighting, sustainable building materials etc. Most Australian homes are not built with our harsh climate in mind (well, bung in an airconditioner and she’ll be right mate) or with an eye to global warming. Developers don’t care, they just want the profit.

- it has always struck me as BIZARRE that this Government does not seem to support the renewable energy industry. The previous Government gave rebates to householders who installed solar power or photovoltaics – we did both and now sell back our unused electricity to the grid. Germany apparently leads the world in renewable energy, yet here we are, a large continent full of sunshine and funding for research into renewable energies has contracted.

- throw squillions of dollars at public schools (and not just for assembly halls) – after all, it’s the kids of the future who will have the skills to seize opportunities, create industries and jobs. At the moment, we are saddling them with enormous future debt.

- set an executive salary cap – not just for companies that are bailed out.

- get tough on banks. Don’t allow banks to get away with not passing on a cut in interest rates and don’t allow them to lend money they simply don’t have.

- get smart about copper – I’ve said before on this blog that copper will be the resource of the future. There’s a black market in copper. It gets stolen from construction sites, off railroad tracks, from household plumbing systems. China is particularly thirsty for copper. Why? The main reason I think is that copper is used in hybrid cars and hybrid cars are the future. The increasing price of fuel and the dramatic impact of fossil fuels on our planet will drive the uptake of hybrids. In 2008, Rudd said that the Government would get behind hybrid car research and development – is this happening or was the intention cast aside by the GFC? Australia is a leading producer of copper with many copper mines, such as the Mt Isa copper mine in Queensland. Chinese companies are busy snapping up mining and energy assets around the world, including copper mines. You only have to peruse Chinalco’s (Chinese resource company and aka Aluminium Corp of China) website to see they already own 100% of Peru’s copper industry. And we know they are salivating at the thought of investing in Rio Tinto who own 30% of the Escondida copper mine in Chile and have agreed to sell 49.5% of that 30% stake to Chinalco. This is a controversial deal that would see Rio Tinto get US$19.5 billion and help repay its huge $US38.7 billion debts from the acquisition of Canadian aluminium giant, Alcan, in 2007. Personally, I’d like to see the Australian Government stop a major source of this country’s wealth from going overseas. Chinalco is not a private corporate; it is a Chinese government-owned company – so any future disputes, say over how a mine is operating, are at a level beyond a corporate cat fight and could affect diplomatic relations between Australia and China. We need to think long and hard about our resources, particularly copper in light of what I’ve suggested, before we open up to foreign investment. Chinese foreign investment is not necessarily the smartest way to ride out the GFC. How does flogging off a mining company or two help unemployment? And another thing: wouldn’t details of Rio Tinto’s pricing structure and negotiations pass into the hands of the Chinese Government and put BHP Billiton into an unfair negotiating position??

These are just some of my questions and thoughts. The issue to me is where to best put Government spending and so far, I don’t think we’re getting much bang for the buck by throwing bonuses at households and praying they will take that money and party at the local shopping mall. What do you think?

UPDATE: June 5 2009: Rio Tinto spurns Chinalco bid due to shareholder protests and will joint with BHP Billiton in an iron ore joint venture.

Let’s shift our focus

For today’s post, I’m bringing you two quotes I’ve found whilst reading on the global financial hissy fit aka GFC. They both say it all really – couldn’t agree more.

For today’s post, I’m bringing you two quotes I’ve found whilst reading on the global financial hissy fit aka GFC. They both say it all really – couldn’t agree more.

First up, from Harry S. Dent (author of The Great Depression Ahead):

“Western world consumers are now spending less. This will last for a number of years. No amount of stimulus, and no waiting period, will cause consumers to rush back to stores and car lots, buying on credit. Not only are consumers spending less, but there has been a shift in goals. It is no longer about what you have (more stuff), but what you don’t have (paying off debt). Add to this an incredible shrinking personal asset base (homes, 401(k)’s, savings accounts, etc.), and you get one more solid reason for consumers to change their focus.”

And then from Bob Waldrop (a libertarian activist and permaculture expert):

“If we don’t stand together against this, the future is bleak. We stand together when we slash our consumption, take our money out of the big transcontinental banks, invest and spend our money in our local economies, plant gardens and grow local food systems and refuse to listen to the lies of politicians and Wall Street sociopaths anymore.”

Invent your own currency

Wall Street financial operators, greedy banks (can you BELIEVE that some Australian banks are refusing to pass on the latest Reserve Bank rate cut?) and the consumerist society treadmill we have all been on for years have all led us to our current sorry state – the Global Financial Hissy Fit or GFC.

Wall Street financial operators, greedy banks (can you BELIEVE that some Australian banks are refusing to pass on the latest Reserve Bank rate cut?) and the consumerist society treadmill we have all been on for years have all led us to our current sorry state – the Global Financial Hissy Fit or GFC.

But here’s a trend I’m liking. Back in the Great Depression, communities in the United States were allowed to print and use their own local currency as long as it didn’t resemble Federal currency. This helped to keep local economies afloat. As communities in 2009 stagger under the impacts of the GFHF and face rising unemployment rates and closing down of businesses, some communities are printing and naming their own currency (also known as complementary currency or regional currency).

Don’t know about you but I don’t have a whole lot of confidence in our current financial system or the bailout packages that are supposed to heave us out of the black hole we’ve dug for ourselves (ably assisted by so-called financial whiz-kids of Wall St).

So if you’re a community facing an unemployment rate of 22.2% and your hometown confidence is heading south, what do you do? Print your own money! A bunch of business dudes in Detroit, for example, have banded together to support local commerce and provide a medium of exchange that can be used for local goods and services. They’ve created the Detroit Cheers and local businesses are agreeing to use it as real money. The Cheers bill comes in $3 denominations. The owner of a furniture shop says:

“I can get a good meal, I can get a beer, I can help another Detroit business. That is money to me. To keep commerce in Detroit, I totally support that goal.”

A dog day care centre, a graphics designer, a carpenter, a nonprofit and several restaurants and bars are participating in the scheme.

I did a spot of research and found this really is an emerging trend in the US because other States have local currencies:

- BerkShares in the Berkshires region of western Massachusetts

- Pittsboro, N.C. is reviving the Plenty, a local currency it used to have

- Bay Buck in Traverse City, Michigan

- Burlington Bread in Burlington, Vermont

- Brooklyn Greenbacks in Brooklyn, N.Y.

- Ithaca Hours in New York (each one equal to either $10 or one hour of work)

Ithaca Hours is printed on good-quality paper with images of steamboats, waterfalls, children and animals. Each one has a serial number and a faint graphic on the currency to discourage counterfeiters (but because the currency is only used and accepted locally, I doubt counterfeiters would be interested). Check out the currency’s website.

From a knowledge management perspective, local currencies help to build social capital – a community preserves and uses its skills and expertise, strengthens local relationships, fosters confidence and faith within the community about its ability to survive and thrive during the worst economic hissy fit we’ve seen since the 1930s; and builds up community resilience. It also gives the local currency a ‘social life”.

I found this so fascinating that I did more research. A whole history of local currencies was revealed. During the Great Depression, the most famous example seems to be the Austrian town of Wörgl, which had the Stamp Scrip. And did you know that in Europe there are 65 local currencies competing with the Euro? The Bavarian region of Chiemgau prints the the Chiemgauer and Devon has the Totnesian pound.

Prior to the American Civil War, the US had no national currency and used local currency issued by banks. Only in 1863, did the US greenback come into existence.

The whole idea of local currencies is connected to Local Exchange Trading Systems (LETS) and I predict we’re going to see a return to community or network members desiring currency or credit (in the form of hours for example) for the benefit of the community and themselves. I don’t think this has to be a rejection of the global capitalist model but it could function as an adjunct to it.

We’ve ended up with money leading us around and we’ve forgotten that the notion of commerce used to be about conversation in the course of bartering and negotiating the exchange of goods and services. It used to be about social intercourse and mutual benefit. Let’s go back to that!

Credit crisis visualised

Whilst trying to come to grips with the global financial crisis, I’ve been reading and researching. Came across this YouTube video, which explains how the credit crisis happened but what’s particularly interesting is that the videos were put together by a Media Design student, Jonathan Jarvis, as part of a thesis project. He wanted to explore the use of new media to make sense of an increasingly complex world.

So he uses animated figures and images to explain in simple, visual terms what the heck happened. Here are the videos for your viewing pleasure (Parts 1 and 2).

We’ve been here before

I’ve become very interested in the Kondratieff Long Wave Cycle or K-cycle and have been looking into all the booms and busts that have taken place over the last 150 years or so. Since WWII, we’ve been living pretty comfortably and times have been prosperous. But when you look back, there have been regular cycles of economic panics and booms. For example, there was a huge panic in 1907 in the US, known as the 1907 Banker’s Panic, which was apparently anticipated around 1910.

I’ve become very interested in the Kondratieff Long Wave Cycle or K-cycle and have been looking into all the booms and busts that have taken place over the last 150 years or so. Since WWII, we’ve been living pretty comfortably and times have been prosperous. But when you look back, there have been regular cycles of economic panics and booms. For example, there was a huge panic in 1907 in the US, known as the 1907 Banker’s Panic, which was apparently anticipated around 1910.

In 1902, a newspaper article, entitled “Panics and Booms” appeared, which frankly describes our economic crisis of today. Written by L.M. Holt in 1897 (at the tail end of the Long Depression in the US) it was republished in 1902 and Holt argues that booms always follow busts. The early 1900s were boom times so the article was a warning to prepare for an upcoming economic hissy fit.

Basically, Holt says that a depression is caused by over-indebtedness and to get out of a depression, we have to pay back the debt (and clearly in our own times that includes bailouts and stimulus packages). The more debt, the longer the economic slump. Here is the 1902 article but you can also read it here. The article is fantastic because it’s such a simple read – no pointy-headed economic jargon or economic formulae.

It’s really worth reading if only to realise that it seems the lesson for each generation is to learn all over again what is within our means and what is not affordable. But do we ever learn? As Holt says:

“Gradually the surplus debts of the country are paid and the people breathe easier again. People live within their incomes and temporarily learn economical habits. Men smoke fewer and cheaper cigars and ladies purchase fewer ribbons and occasionally fix over a bonnet and dress instead of getting new ones.”

So when we recover from the GFC, our collective task will be to stick with the “economical habits” we will surely have to adopt to survive the GFC and we will have to learn the hard lesson of not getting sucked up in over-indebtedness again.

She’ll be right mate! (we hope)

The global financial hissy fit is hitting Australia. We are not immune, despite this country having rich, natural resources. You need a country or two to buy these natural resources and if those countries (like China) are feeling pain, well, you ‘aint going to sell as much as you think. What happens is that these countries come after your natural resources, hoping to get them at bargain basement prices – so, for example, Chinalco has an AU$30 billion bid for 18% of Rio Tinto (although I suspect the Foreign Investment Review Board will block this).

The global financial hissy fit is hitting Australia. We are not immune, despite this country having rich, natural resources. You need a country or two to buy these natural resources and if those countries (like China) are feeling pain, well, you ‘aint going to sell as much as you think. What happens is that these countries come after your natural resources, hoping to get them at bargain basement prices – so, for example, Chinalco has an AU$30 billion bid for 18% of Rio Tinto (although I suspect the Foreign Investment Review Board will block this).

Our national unemployment rate has risen from 4.8% to 5.2% on the heels of 590,000 people being tossed out of a job. Australian banks are ditching their employees overboard and moving jobs to India. Pacific Brands (the company behind labels like Bonds, Holeproof, Berlei and Hard Yakka) has closed seven of its Australian factories and axed 1850 jobs (which will be sent offshore as part of its restructuring plan). In a day of horror, 3565 jobs were lost when BHP Billiton, Rio Tinto, David Jones and CSR took the razor to their workforces.

Our PM is saying: “Things will get worse before they get better ….The magnitude of the global financial crisis almost beggars belief.”

But I was having lunch with a chap the other day and this person said: “Global recession? What recession? People are still lunching and buying things. She’ll be right mate!” Ah, yes the good old Aussie national response to anything that looks as though it might disrupt our obsession with footy, meat pies, Holden cars or retail therapy. This response has always struck me as about as dumb as sticking your head in the sand. Alternatively, we could say it’s the Aussie fighting spirit – that we’re a nation of tough as boots people who endure harsh weather, droughts, floods, bushfires, you name it. So a global financial hissy fit isn’t going to scare us one bit. Bring it on!

But pause for thought: I had to travel to Melbourne earlier this week to facilitate a meeting and in the hotel room was a copy of The Week (Australian edition, March 13 2009). I’d been reading Harry S Dent’s book, The Great Depression Ahead, and was too forlorn to continue onto Chapter 7 that evening. So I picked up the mag and it opened magically to page 3, where my eye immediately caught sight of this quote (by David Salter):

“What worries me is that when the bad times arrive, which they surely must, we might not turn out to be quite as resilient as we thought. Australians today aren’t the same stoic bunch as those who faced the Great Depression. For them, Gallipoli and the horrors of the Western Front were just 15 years earlier. Many of the tough men and women who’d survived the terrible drought and financial hardships of the 1890s still sat at the head of family tables. We’re much softer now – coddled by welfare entitlements and high standards of living based on personal debt. Will we still have the reserves of tenacity, endurance and self-sacrifice to match our grandparents?”.

And THIS I think is the profound question that will face Australians in 2009 and 2010. As a nation, do we still have the right stuff to weather the vicious storm ahead?

How do you define “Depression”?

Now, you know I am no pointy-headed economist, so I’ve been doing a LOT of reading on the GFC or global financial hissy fit as I prefer to call it. Interesting to see our current financial mess has its very own acronym. Hopefully, one day soon we can say LOL GFC – because we’ll experience an upturn.

Now, you know I am no pointy-headed economist, so I’ve been doing a LOT of reading on the GFC or global financial hissy fit as I prefer to call it. Interesting to see our current financial mess has its very own acronym. Hopefully, one day soon we can say LOL GFC – because we’ll experience an upturn.

But cast your eye over the ThinkingShift Book Club on the right panel of this blog – see the book I’m reading? It’s freaking me out frankly. Basically, it says late 2009 or early 2010 we’re all doomed as the Big D will hit us. Big D being Depression, major financial drama. I’ll do a future post and let you know what the book says but with all the talk of the Big D, it did prompt me to wander off and find out how a Depression is defined.

As I understand it: a Depression can be recognised by changes in the Gross Domestic Product (GDP). The GDP is the total value of goods and services produced within a country’s physical borders during a period of time (usually one fiscal year). GDP excludes net income from abroad. So apparently you know you’re in the icy grip of a Depression when real GDP declines by 10% or more. Anything else, it’s a Recession. I read somewhere that this distinction had to be made because prior to THE depression of the 1930s, any economic downturn was referred to as a depression, so economists named smaller economic declines “recessions”.

So far so good. During the last major economic drama in 1982, when we teetered on The Edge of the Big D, GDP fell by 3%, so it didn’t reach that magical 10% threshhold. So let’s look at the current GFC – is there a 10% GDP decline and are we about to teeter off The Edge? Yeah, well it ‘aint good news.

The Wall Street Journal is talking prophecies of doom and darkness saying:

“The bottom line is that there is ample reason to worry about slipping into a depression. There is a roughly one-in-five chance that U.S. GDP and consumption will fall by 10% or more, something not seen since the early 1930s.”

Mmmm….my cunning mathematical ability tells me that’s a 20% chance of slipping off The Edge. The article was written by a professor of Economics so guess he has a better idea than most of us about what’s going to happen. Research apparently shows that depressions are closely associated with stockmarket crashes like we’ve just witnessed. So there’s an increased chance of a depression looming when the stockmarket goes haywire. So of course the 1930s Depression was accompanied by a stockmarket crash of 55%. And the WSJ research uncovered 71 cases of stockmarket crashes that were followed by depressions.

In fact, looking at 34 countries, research shows that there is a 28% probability that a “minor depression” (macroeconomic decline of 10% or more) will occur when there is a stock-market crash. And there is a 9% chance that a “major depression” (a fall of 25% or more) will occur when there is a stock-market crash. I thought a depression was a depression, full stop/period. Didn’t realise there are minor and major depressions.

More interestingly, there is a 73% probability that a “minor depression” will also feature a stock-market crash whilst for a “major depression” to be accompanied by a stock-market crash, the probability is 92%.

I’m sure this was not meant to be humorous but the WSJ article finishes off by saying:

“The odds are roughly one-in-five that the current recession will snowball into the macroeconomic decline of 10% or more that is the hallmark of a depression. The bright side of a 20% depression probability is the 80% chance of avoiding a depression.”

Okay, so I’m hanging on to the 80% bright and happy statistic. But when I stick my nose in Harry S Dent’s book, The Great Depression Ahead, I’m afraid he’s not so optimistic. I’ll bring you what Dent has to say in a future post.

Made in New Zealand

Made in New Zealand

{kind=link}